What is Forex?

Quite simply, it’s the global financial market that allows one to trade currencies.

If you think one currency will be stronger versus the other, and you end up correct, then you can make a profit.

Learn moreQuite simply, it’s the global financial market that allows one to trade currencies.

If you think one currency will be stronger versus the other, and you end up correct, then you can make a profit.

Learn moreThe simple answer is MONEY. Specifically, currencies.

Because you’re not buying anything physical, forex trading can be confusing so we’ll use a simple (but imperfect) analogy to help explain.

Learn moreThe biggest appeal that forex trading offers is the ability to trade on margin.

But for many forex traders, “margin” is a foreign concept and one that is often misunderstood.

Learn moreForex brokers will quote you two different prices for a currency pair: the bid and ask price.

The “bid” is the price at which you can SELL the base currency.

Learn moreWhen trading forex, you are only required to put up a small amount of capital to open and maintain a new position.

This capital is known as the margin.

Learn moreIn order to understand what Used Margin is, we must first understand what Required Margin is.

Whenever you open a new position, a specific amount of Required Margin is set aside.

Learn moreThe account equity or simply “Equity” represents the current value of your trading account.

Equity is the current value of the account and fluctuates with every tick when looking at your trading platform on your screen.

Learn moreCryptocurrencies have become extremely popular in recent years. Not just online, but everywhere.

You’ve probably even seen TV commercials about cryptocurrencies being the next big thing. And maybe even your favourite actor or athlete promoting them.

Learn moreWhy is it often hailed as a game-changer in the world of money?

As mentioned in an earlier lesson, a mysterious figure who called himself, Satoshi Nakamoto authored a white paper titled, Bitcoin: A Peer-to-Peer Electronic Cash System.

Learn moreWhat’s the difference between uppercase “B” and lowercase “b” in Bitcoin?

Learn moreIn the beginning, there was only Bitcoin, created by Satoshi Nakamoto. But due to the open source nature of Bitcoin’s source code, this didn’t last.

Learn moreIf you’ve read the previous lessons from my “Beginner’s Guide to Bitcoin Wallets”, you’ve learned what a crypto wallet is, how to set one up, and how to send and receive bitcoin.

Learn moreCentralised crypto exchanges (CEX) operate in different countries and support different local (fiat) currencies and different cryptocurrencies.

But they all work in similar ways.

Learn moreSelf-sabotage and negative thinking are common psychological obstacles that traders face, often undermining their performance and success in the market.

Learn moreOne of the questions traders always ask me is how important trading psychology is to a newbie.

Learn moreAnalyst

What is an analyst?

What are the different types of analysts?

Equity Analysts

Quite simply, it’s the global financial market that allows one to trade currencies.

If you think one currency will be stronger versus the other, and you end up correct, then you can make a profit.

Once upon a time, before a global pandemic happened, people could actually get on airplanes and travel internationally.

If you’ve ever traveled to another country, you usually had to find a currency exchange booth at the airport, and then exchange the money you have in your wallet into the currency of the country you are visiting.

You go up to the counter and notice a screen displaying different exchange rates for different currencies.

An exchange rate is the relative price of two currencies from two different countries.

You find “Japanese yen” and think to yourself, “WOW! My one dollar is worth 100 yen?! And I have ten dollars! I’m going to be rich!!!”

When you do this, you’ve essentially participated in the forex market!

You’ve exchanged one currency for another.

Or in forex trading terms, assuming you’re an American visiting Japan, you’ve sold dollars and bought yen.

Before you fly back home, you stop by the currency exchange booth to exchange the yen that you miraculously have remaining (Tokyo is expensive!) and notice the exchange rates have changed.

It’s these changes in the exchange rates that allow you to make money in the foreign exchange market.

The foreign exchange market, which is usually known as “forex” or “FX,” is the largest financial market in the world.

The FX market is a global, decentralized market where the world’s currencies change hands. Exchange rates change by the second so the market is constantly in flux.

Only a tiny percentage of currency transactions happen in the “real economy” involving international trade and tourism like the airport example above.

Instead, most of the currency transactions that occur in the global foreign exchange market are bought (and sold) for speculative reasons.

Currency traders (also known as currency speculators) buy currencies hoping that they will be able to sell them at a higher price in the future.

Compared to the “measly” $200 billion per day volume of the New York Stock Exchange (NYSE), the foreign exchange market looks absolutely ginormous with its $6.6 TRILLION a day trade volume.

That’s trillion with a “t”.

Let’s take a moment to put this into perspective using monsters…

The largest stock market in the world, the New York Stock Exchange (NYSE), trades a volume of about $200 billion each day. If we used a monster to represent the NYSE, it would look like this…

Looks intimidating. Looks like it works out. Some may even find it sexy.

You hear about the NYSE in the news every day… on CNBC… on Bloomberg…on BBC… heck, you even probably hear about it at your local gym. “The NYSE is up today, blah, blah”.

When people talk about the “market”, they usually mean the stock market. So the NYSE sounds big, it’s loud and likes to make a lot of noise.

But if you actually compare it to the forex market, it would look like this…Oooh, the NYSE looks so puny compared to the forex market! It doesn’t stand a chance!

Makes you wonder if the “S” in NYSE stands for “Stock” or for “Scrawny”? 🤣

The cryptocurrency market is even punier.

Check out the graph of the average daily trading volume for the forex market, New York Stock Exchange, Tokyo Stock Exchange, and London Stock Exchange:

The currency market is over 200 times BIGGER! It is HUGE!

But hold your horses, there’s a catch!

That huge $6.6 trillion number covers the entire global foreign exchange market, BUT the “spot” market, which is the part of the currency market that’s relevant to most forex traders is smaller at $2 trillion per day.

And then, if you just want to count the daily trading volume from retail traders (that’s us), it’s even smaller.

It is very difficult to determine the exact size of the retail segment of the FX market, but it’s estimated to be around 3-5% of overall daily FX trading volumes, or around $200-300 billion (probably less).

So you see, the forex market is definitely huge, but not as huge as the others would like you to believe.

Don’t believe the “forex is a $6.6 trillion market” hype! The huge number sounds impressive, but a bit misleading. We don’t like to exaggerate. We just keepin’ it real.

Aside from its size, the market also rarely closes! It’s open virtually round the clock.

The forex market is open 24 hours a day and 5 days a week, only closing down during the weekend. (What a bunch of slackers!)

The simple answer is MONEY. Specifically, currencies. Because you’re not buying anything physical, forex trading can be confusing so we’ll use a simple (but imperfect) analogy to help explain. Think of buying a currency as buying a share in a particular country, kinda like buying shares in a company. The price of the currency is usually a direct reflection of the market’s opinion on the current and future health of its respective economy. In forex trading, when you buy, say, the Japanese yen, you are basically buying a “share” in the Japanese economy.

You are betting that the Japanese economy is doing well, and will even get better as time goes. Once you sell those “shares” back to the market, hopefully, you will end up with a profit. In general, the exchange rate of a currency versus other currencies is a reflection of the condition of that country’s economy, compared to other economies. By the time you graduate from this School of Pipsology, you’ll be eager to start working with currencies.

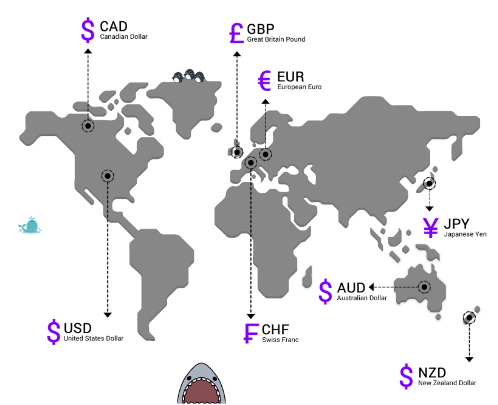

Major CurrenciesWhile there are potentially lots of currencies you can trade, as a new forex trader, you will probably start trading with the “major currencies“.

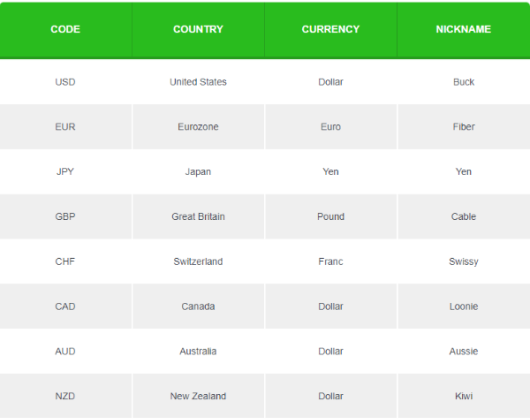

They’re called “major currencies” because they’re the most heavily traded currencies and represent some of the world’s largest economies. Forex traders differ on what they consider as “major currencies”. The uptight ones who probably got straight A’s and followed all the rules as children only consider USD, EUR, JPY, GBP, and CHF as major currencies. Then they label AUD, NZD, and CAD as “commodity currencies“. For us rebels, and to keep things simple, we just consider all eight currencies as the “majors”. Below, we list them by their symbol, country where they’re used, currency name, and cool nicknames.

Currency symbols always have three letters, where the first two letters identify the name of the country and the third letter identifies the name of that country’s currency, usually the first letter of the currency’s name. These three letters are known as ISO 4217 Currency Codes. By 1973, the International Organization for Standardization (ISO) established the three-letter codes for currencies that we use today.

Take NZD for instance…

NZ stands for New Zealand, while D stands for dollar.

Easy enough, right?

The currencies included in the chart above are called the “majors” because they are the most widely traded ones.

We’d also like to let you know that “buck” isn’t the only nickname for USD.

There’s also: greenbacks, bones, benjis, benjamins, cheddar, paper, loot, scrilla, cheese, bread, moolah, dead presidents, and cash money.

So, if you wanted to say, “I have to go to work now.”

Instead, you could say, “Yo, I gotta bounce! Gotta make them benjis son!”

Bob sure knows his fried chicken and mashed potatoes but absolutely has no clue about margin and leverage.

Margin trading gives you the ability to enter into positions larger than your account balance.

With a little bit of cash, you can open a much bigger trade in the forex market.

And then with just a small change in price moving in your favor, you have the possibility of ending up with massively huge profits.

But for most new traders, because they usually don’t know what they’re doing, that’s not what usually happens.

More likely, price does move, but it moves against them. Like what happened to Bob.

Bob was in a trade.

He was sure that this trade was going to be a winner so he bet BIG.

All of a sudden, to Bob’s surprise (and shock), he witnessed his trade being automatically closed on his trading platform and ended up suffering an epic loss.

The funds that now remain in Bob’s account aren’t even enough to open another trade.

Bob is confused. He asks himself, “WTF just happened?”

Bob sure knows his fried chicken and mashed potatoes but absolutely has no clue about margin and leverage.

Margin trading gives you the ability to enter into positions larger than your account balance.

With a little bit of cash, you can open a much bigger trade in the forex market.

And then with just a small change in price moving in your favor, you have the possibility of ending up with massively huge profits.

But for most new traders, because they usually don’t know what they’re doing, that’s not what usually happens.

More likely, price does move, but it moves against them. Like what happened to Bob.

Bob was in a trade.

He was sure that this trade was going to be a winner so he bet BIG.

All of a sudden, to Bob’s surprise (and shock), he witnessed his trade being automatically closed on his trading platform and ended up suffering an epic loss.

The funds that now remain in Bob’s account aren’t even enough to open another trade.

Bob is confused. He asks himself, “WTF just happened?”

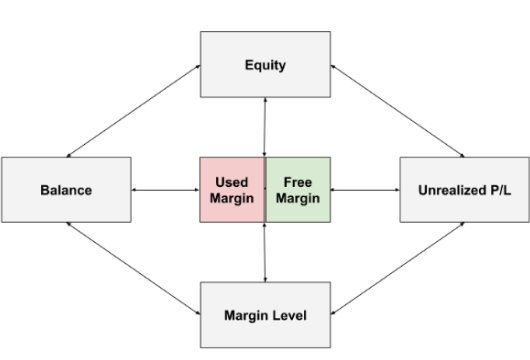

The metriics above are all intertwined.

A change in one causes a change in another.

As a trader, you need to be aware of the relationships between them…

BEFORE ever entering a single trade on a live account.

Don’t be like Bob.

Where certain metrics fall below a certain value, BAD THINGS will happen!

So you need to know what these metrics are!

You also need to know what these “bad things” are!

Make sure you have a solid grasp of how your trading account actually works and how it uses margin.

So let’s dive right in.

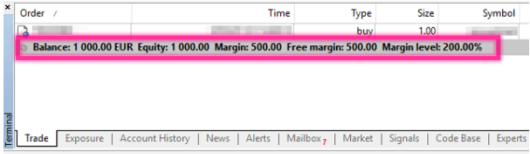

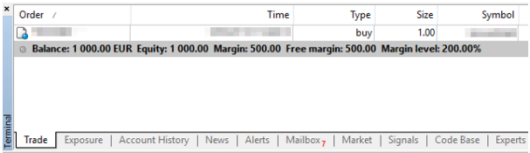

A margin trading account displays the following metrics:

A metric is just a measurement of “something”. This means that every metric above measures something important about your account involving margin. For example, the “Balance” measures how much cash you have in your account. And if you don’t have a certain amount of cash, you may not have enough “margin” to open new trades or keep existing trades open. Depending on the trading platform, each metric might have slightly different names but what’s being measured is the same. Let’s take another look at the metrics on MetaTrader 4.

You’ll notice that it looks like “Used Margin” is not displayed. But it’s there. MetaTrader 4 just displays it as “Margin”.

Here’s another example of account metrics from a different forex trading platform:

Same metrics as MetaTrader 4, but different labels.

Don’t worry about the different labels right now, we’ll explain each margin-related metric in a way that you’ll be able to know which metric is which regardless of the exact label.

We’ll also let you know what other names that a specific metric is also known by. And at the end of this Margin Trading 101 course, we’ll provide a helpful “cheat sheet” for all this margin jargon.

Let’s now discuss each metric one-by-one in detail.

We’ll start with an easy one…

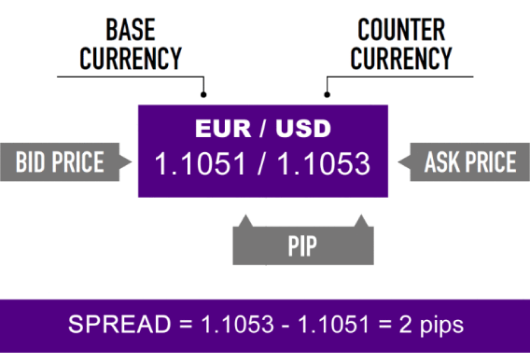

Forex brokers will quote you two different prices for a currency pair: the bid and ask price.

The “bid” is the price at which you can SELL the base currency.

The “ask” is the price at which you can BUY the base currency.

The difference between these two prices is known as the spread.

Also known as the “bid/ask spread“.

The spread is how “no commission” brokers make their money.

This spread is the fee for providing transaction immediacy.

This is why the terms “transaction cost” and “bid-ask spread” are used interchangeably.

Instead of charging a separate fee for making a trade, the cost is built into the buy and sell price of the currency pair you want to trade.

From a business standpoint, this makes sense. The broker provides a service and has to make money somehow.

It’s just like if you were trying to sell your old iPhone to a store that buys used iPhones. (A smartphone with only two rear cameras? Yuck!)

In order to make a profit, it will need to buy your iPhone at a price lower than the price it’ll sell it for.

If it can sell the iPhone for $500, then if it wants to make any money, the most it can buy from you is $499.

That difference of $1 is the spread.

So when a broker claims “zero commissions” or “no commission”, it’s misleading because while there is no separate commission fee, you still pay a commission.

How is the Spread in Forex Trading Measured?The spread is usually measured in pips, which is the smallest unit of the price movement of a currency pair. For most currency pairs, one pip is equal to 0.0001. An example of a 2 pip spread for EUR/USD would be 1.1051/1.1053.

Currency pairs involving the Japanese yen are quoted to only 2 decimal places (unless there are fractional pips, then it’s 3 decimals). For example, USD/JPY would be 110.00/110.04. This quote indicates a spread of 4 pips.

What Types of Spreads are in Forex?The type of spreads that you’ll see on a trading platform depends on the forex broker and how they make money.

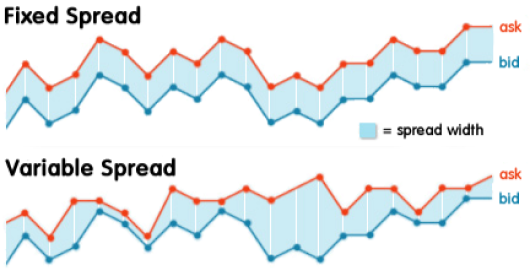

There are two types of spreads:

1. Fixed

2. Variable (also known as “floating”)

Fixed spreads are usually offered by brokers that operate as a market maker or “dealing desk” model while variable spreads are offered by brokers operating a “non-dealing desk” model.

What are Fixed Spreads in Forex?Fixed spreads stay the same regardless of what market conditions are at any given time.

In other words, whether the market is volatile like Kanye’s moods or quiet as a mouse, the spread is not affected. It stays the same.

Fixed spreads are offered by brokers that operate as a market maker or “dealing desk” model.

Using a dealing desk, the broker buys large positions from their liquidity provider(s) and offers these positions in smaller sizes to traders.

This means that the broker acts as the counterparty to their clients’ trades.

Having a dealing desk, allows the forex broker to offer fixed spreads because they are able to control the prices they display to their clients.

What are the Advantages of Trading With Fixed Spreads?Fixed spreads have smaller capital requirements, so trading with fixed spreads offers a cheaper alternative for traders who don’t have a lot of money to start trading with.

Trading with fixed spreads also makes calculating transaction costs more predictable.

Since spreads never change, you’re always sure of what you can expect to pay when you open a trade.

Requotes can occur frequently when trading with fixed spreads since pricing is coming from just one source (your broker).

And by frequently, we mean almost as frequently as Instagram posts from Kardashian sisters!

There will be times when the forex market is volatile and prices are rapidly changing. Since spreads are fixed, the broker won’t be able to widen the spread to adjust for current market conditions.

So if you try to enter a trade at a specific price, the broker will “block” the trade and ask you to accept a new price. You will be “re-quoted” with a new price.

The requote message will appear on your trading platform letting you know that price has moved and asks you whether or not you are willing to accept that price. It’s almost always a price that is worse than the one you ordered.

Slippage is another problem. When prices are moving fast, the broker is unable to consistently maintain a fixed spread and the price that you finally end up after entering a trade will be totally different than the intended entry price.

Slippage is similar to when you swipe right on Tinder and agree to meet up with that hot gal or guy for coffee and realize the actual person in front of you looks nothing like the photo.

What are Variable Spreads in Forex?As the name suggests, variable spreads are always changing.

With variable spreads, the difference between the bid and ask prices of currency pairs is constantly changing.

Variable spreads are offered by non-dealing desk brokers.

Non-dealing desk brokers get their pricing of currency pairs from multiple liquidity providers and pass on these prices to the trader without the intervention of a dealing desk.

This means they have no control over the spreads.

And spreads will widen or tighten based on the supply and demand of currencies and the overall market volatility.

Typically, spreads widen during economic data releases as well as other periods when the liquidity in the market decreases (like during holidays and when the zombie apocalypse begins).

What are the Advantages of Trading With Variable Spreads?Variable spreads eliminate experiencing requotes. This is because the variation in the spread factors in changes in price due to market conditions.

(But just because you won’t get requoted doesn’t mean you won’t experience slippage.)

Trading forex with variable spreads also provides more transparent pricing, especially when you consider that having access to prices from multiple liquidity providers usually means better pricing due to competition.

What are the Disadvantages of Trading With Variable Spreads?

Variable spreads aren’t ideal for scalpers. The widened spreads can quickly eat into any profits that the scalper makes.

Variable spreads are just as bad for news traders. Spread may widen so much that what looks like a profitable can turn into an unprofitable within a blink of an eye.

Fixed vs Variable Spreads: Which is Better?The question of which is a better option between fixed and variable spreads depends on the needs of the trader.

There are traders who may find fixed spreads better than using variable spread brokers. The reverse may also be true for other traders.

Generally speaking, traders with smaller accounts and who trade less frequently will benefit from fixed spread pricing.

And traders with larger accounts who trade frequently during peak market hours (when spreads are the tightest) will benefit from variable spreads.

Traders who want fast trade execution and need to avoid requotes will want to trade with variable spreads.

Spread Costs and CalculationsNow that you know what a spread is, and the two different types of spreads, you need to know one more thing…

How the spread relates to actual transaction costs.

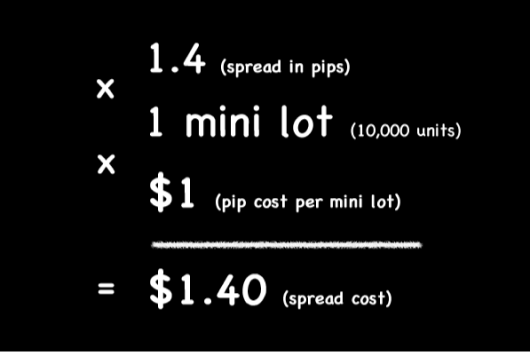

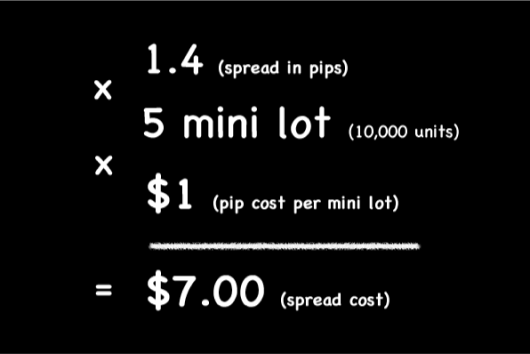

In the quote above, you can buy EURUSD at 1.35640 and sell EURUSD at 1.35626.

This means if you were to buy EURUSD and then immediately close it, it would result in a loss of 1.4 pips.

To figure out the total cost, you would multiply the cost per pip by the number of lots you’re trading.

So if you’re trading mini lots (10,000 units), the value per pip is $1, so your transaction cost would be $1.40 to open this trade.

The pip cost is linear. This means that you will need to multiply the cost per pip by the number of lots you are trading.

If you increase your position size, your transaction cost, which is reflected in the spread, will rise as well.

For example, if the spread is 1.4 pips and you’re trading 5 mini lots, then your transaction cost is $7.00.

When trading forex, you are only required to put up a small amount of capital to open and maintain a new position. This capital is known as the margin.

For example, if you want to buy $100,000 worth of USD/JPY, you don’t need to put up the full amount, you only need to put up a portion, like $3,000. The actual amount depends on your forex broker or CFD provider.

Margin can be thought of as a good faith deposit or collateral that’s needed to open a position and keep it open. It is a “good faith” assurance that you can afford to hold the trade until it is closed.

Margin is NOT a fee or a transaction cost. Margin is simply a portion of your funds that your forex broker sets aside from your account balance to keep your trade open and to ensure that you can cover the potential loss of the trade.

This portion is “used” or “locked up” for the duration of the specific trade. Once the trade is closed, the margin is “freed” or “released” back into your account and can now be “usable” again… to open new trades.

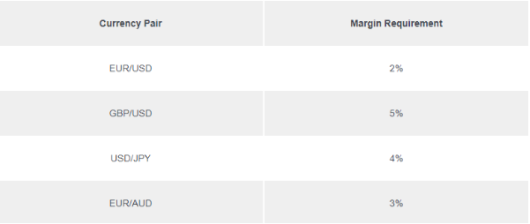

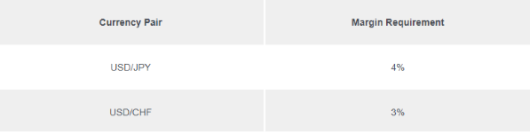

What is Margin Requirement?Margin is expressed as a percentage (%) of the “full position size”, also known as the “Notional Value” of the position you wish to open. Depending on the currency pair and forex broker, the amount of margin required to open a position VARIES. You may see margin requirements such as 0.25%, 0.5%, 1%, 2%, 5%, 10% or higher. This percentage (%) is known as the Margin Requirement. Here are some examples of margin requirements for several currency pairs:

What is Required Margin?

What is Required Margin?

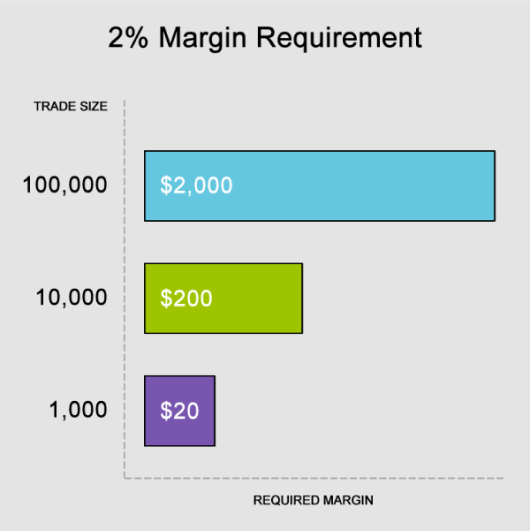

When margin is expressed as a specific amount of your account’s currency, this amount is known as the Required Margin. EACH position you open will have its own Required Margin amount that will need to be “locked up”. Let’s look at a typical EUR/USD (euro against U.S. dollar) trade. To buy or sell a 100,000 of EUR/USD without leverage would require the trader to put up $100,000 in account funds, the full value of the position. But with a Margin Requirement of 2%, only $2,000 (the “Required Margin“) of the trader’s funds would be required to open and maintain that $100,000 EUR/USD position.

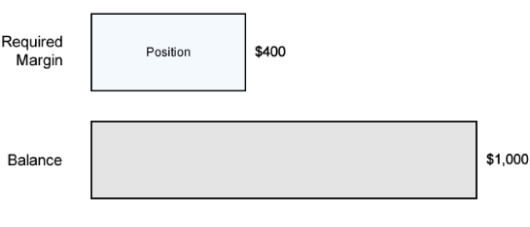

Example #1: Open a long USD/JPY position

Let’s say you’ve deposited $1,000 in your account and want to go long USD/JPY and want to open 1 mini lot (10,000 units) position. How much margin will you need to open this position?

Since USD is the base currency. this mini lot is 10,000 dollars, which means the position’s Notional Value is $10,000. Assuming your trading account is denominated in USD, since the Margin Requirement is 4%, the Required Margin will be $400.

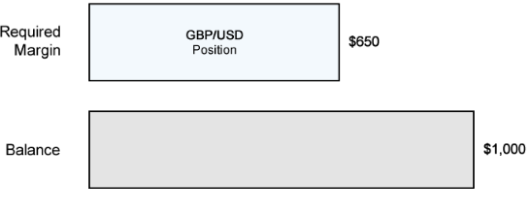

Example #2: Open a long GBP/USD position

Let’s say you’ve deposited $1,000 in your account and want to go long GBP/USD at 1.30000 and want to open 1 mini lot (10,000 units) position. How much margin will you need to open this position? Since GBP is the base currency, this mini lot is 10,000 pounds, which means the position’s Notional Value is $13,000. Assuming your trading account is denominated in USD, since the Margin Requirement is 5%, the Required Margin will be $650.

Example #3: Open a long EUR/AUD position

Let’s say you want to go long EUR/AUD and want to open 1 mini lot (10,000 units) position. How much margin will you need to open this position?

Assuming your trading account is denominated in USD, you need to first know the EUR/USD price. Let’s say EUR/USD is trading at 1.15000. Since EUR is the base currency, this mini lot is 10,000 euros, which means the position’s Notional Value is $11,500. Since the Margin Requirement is 3%, the Required Margin will be $345.

The only reason for having funds in your account is to make sure you have enough margin to use for trading. When it comes to trading forex, your ability to open trades is not necessarily based on the funds in your account balance. More accurately, it’s based on the amount of margin you have. This means that your broker is always looking to see if you have enough margin in your account, which can actually differ from your account balance. If this sounds confusing, don’t you worry. It’ll start to make more sense as we proceed.

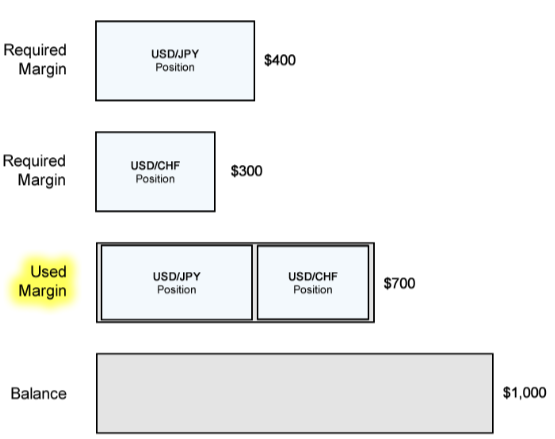

In order to understand what Used Margin is, we must first understand what Required Margin is.

Whenever you open a new position, a specific amount of Required Margin is set aside.

Required Margin was discussed in detail in the previous lesson, so if you don’t know what it is, please read our What is Margin? lesson first.

If you open more than one position at a time, each specific position will have its own Required Margin.

If you add up all of the Required Margin of all the positions that are open, the total amount is what’s called the Used Margin.

Used Margin is all the margin that’s “locked up” and can’t be used to open new positions.

This margin is already being “used”. Hence the name, Used Margin.

While Required Margin is tied to a SPECIFIC trade, Used Margin refers to the amount of money you needed to deposit to keep ALL your trades open.

Example: Open a long USD/JPY and USD/CHF position

Let’s say you’ve deposited $1,000 in your account and want to open TWO positions:

The Margin Requirement for each currency pair is as follows:

How much margin (“Required Margin”) will you need to open each position?

Since USD is the base currency for both currency pairs. A mini lot is 10,000 dollars, which means EACH position’s notional value is $10,000.

Let’s now calculate the Required Margin for EACH position.

USD/JPY PositionThe Margin Requirement for USD/JPY is 4%. Assuming your trading account is denominated in USD, the Required Margin will be $400.

USD/CHF Position

USD/CHF Position

The Margin Requirement for USD/CHF is 3%.

Assuming your trading account is denominated in USD, the Required Margin will be $300.

Since you have TWO trades, the Used Margin in your trading account will be $700.

The account equity or simply “Equity” represents the current value of your trading account.

Equity is the current value of the account and fluctuates with every tick when looking at your trading platform on your screen. It is the sum of your account balance and all floating (unrealized) profits or losses associated with your open positions.

As your current trades rise or fall in value, so does your Equity.

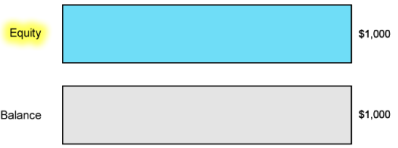

How to Calculate Equity If You Have No Trades OpenIf you do NOT have any open positions, then your Equity is the same as your Balance.

Example: Account Equity When You Have No Open Trades

You deposit $1,000 in your trading account.

Since you haven’t opened any trades yet, your Balance and Equity is the same.

How to Calculate Equity If You Have Trades Open

How to Calculate Equity If You Have Trades Open

If you have open positions, your Equity is the sum of your account balance and your account’s floating P/L.

Example: Account Equity When an Existing Trade is Losing

You deposit $1,000 in your trading account.

Beyoncé tweets that she’s shorting GBP/USD. Because she’s Beyoncé, you follow what she says and go short also.

Price moves immediately against you and your trade shows a floating loss of $50.

The Equity in your account is now $950

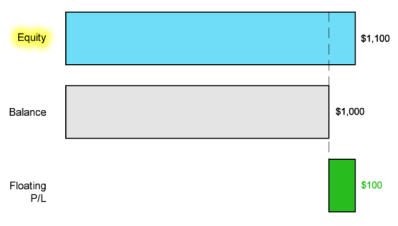

Example: Account Equity When an Existing Trade is Winning

Beyoncé tweets again and says she’s changed her mind. She’s now long GBP/USD.

Not only is she Crazy in Love, but she seems crazy in trading also.

But because she’s the Queen B, you follow what she says and go long also.

Price moves immediately in your favour and your trade shows a floating gain of $100.

What is the difference between Balance and Equity?Let’s start with a simple answer.

If your account is “flat” or does NOT have any positions open, then your Balance and Equity are the SAME.

But if you do have open positions, this is when the Balance and Equity differ.

The Balance reflects your profit/loss from closed positions.

The Equity reflects the real-time calculation of your profit/loss. The Equity takes into account both open AND closed positions.

This means that when you’re looking at your Balance, it is NOT the actual real-time amount of your funds.

Since Equity includes current profits or losses from open trades, it is Equity that shows the real-time amount of your funds.

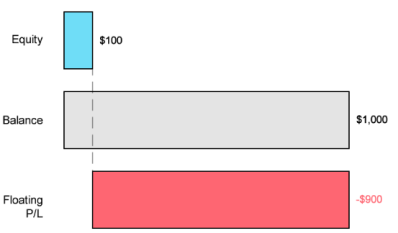

It’s possible to have a very large Balance, but very small Equity.

This happens when your open positions have large unrealized (floating) losses.

For example, if your Balance is $1,000, and you have an open trade that has a floating loss of $900.

Your Equity is only $100.

Cryptocurrencies have become extremely popular in recent years. Not just online, but everywhere.

You’ve probably even seen TV commercials about cryptocurrencies being the next big thing. And maybe even your favourite actor or athlete promoting them.

But what are they?

How are they different from traditional currencies? What makes them so special?

What are cryptocurrencies?A cryptocurrency (or “crypto”) is an umbrella term for a new kind of “digital money” that relies on a combination of technologies that allows it to exist outside the control of central authorities like governments and banks.

Cryptocurrencies are digital.Cryptocurrencies have no physical form. There are no dollar bills or metal coins.

They are completely digital, meaning they’re literally just lines of computer code.

Cryptocurrencies are borderless.

Cryptocurrencies are borderless.

Regardless of where you live or who you are, you can send it almost instantaneously to others anywhere in the world, without concern for geographic distance and country borders.

Cryptocurrencies are borderless. All you need is a device, like a phone or a computer, that’s connected to the internet.

Cryptocurrencies are permissionless.Anybody can send and receive cryptocurrencies. You don’t need to register an account or fill out an application. Cryptocurrencies are permissionless. You don’t even need to give your name. Instead of names and account numbers, all you need to provide is a computer-generated string of letters and numbers known as an “address”. This address is not inherently tied to any of your personal information, so you can theoretically send cryptocurrencies to other people without ever knowing each other’s actual identities. Since you can send and receive cryptocurrencies without giving any personally identifying information, cryptocurrencies provide some degree of privacy.

Cryptocurrencies are decentralised.Unlike traditional currencies, also known as “fiat” currencies, such as the U.S. dollar, cryptocurrencies are not connected to any government or central bank.

For example, the U.S. dollar is issued and controlled by the Federal Reserve (“Fed”), the euro by the European Central Bank (ECB), and the Japanese yen by the Bank of Japan (BOJ).

This means that, unlike fiat currencies, cryptocurrencies are not controlled by a central authority. There is no bank or government behind them. This defining feature of cryptocurrencies is known as decentralisation. If no central bank or government issues or creates cryptocurrencies, then who creates them? Units of a cryptocurrency are generated based on predetermined rules written in code which are executed by software.

One of the most important aspects of cryptocurrencies is their supply since this heavily determines their utility and value.

Depending on the rules written in the code of the software, cryptocurrencies can be created and destroyed.

Some cryptocurrencies have a finite (or fixed) total supply, meaning that there is a maximum number of units that will ever be in circulation, creating scarcity.

Others are launched with an infinite total supply, meaning there is no maximum cap! (Although there might be a limit on the number of new units that can be created within a certain timeframe such as on a yearly basis.)

Cryptocurrencies are counterfeit-proof.

Cryptocurrencies are also designed to be counterfeit-proof.This is where cryptography is involved and how it’s used to securely record and store transactions.

In cryptography, the prefix “crypt” means “hidden” and the suffix “graphy” means “writing”.

But in the modern age, cryptography is now associated with protecting computer information using fancy math.

Since cryptocurrencies rely on cryptography for their security, that’s where the ”crypto” comes from in “cryptocurrencies.”

What makes cryptocurrencies special?Cryptocurrencies exist independently from any government, central bank, or other central institution.

In summary, cryptocurrencies are special because:

Due to these special characteristics, cryptocurrencies provide the potential to give people total control of their money with zero involvement from a third party.

Whether crypto can live up to this potential remains to be seen. Its popularity in the financial world is growing and is now considered an emerging asset class.

Why is it often hailed as a game-changer in the world of money?

As mentioned in an earlier lesson, a mysterious figure who called himself, Satoshi Nakamoto authored a white paper titled, Bitcoin: A Peer-to-Peer Electronic Cash System.

The paper revealed details of creating “electronic cash” (digital currency) free of control from any organisation or government.

During Satoshi Nakamoto’s research though, he discovered there have been multiple attempts in the past to create a digital currency.

There were early pioneers such as b-money, Bit Gold, ecash, E-gold, Hashcash, Liberty Reserve, and RPOW. But they didn’t work out for two main reasons:

So even before Bitcoin was a twinkle in Satoshi’s eye, several attempts have been made to create decentralised electronic money, or digital cash, in the past, but they all failed. 😔

For a while, it seemed impossible.

Unlike a photo, PDF, or other documents, you can’t simply attach some money to an email and send it to someone.

Why?

Because whenever you do a transfer of VALUE between two people, you need to make sure that a real transfer has taken place.

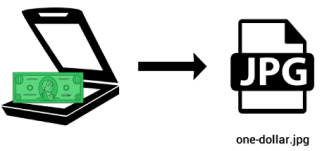

For example, let’s say you ran into the Gingerbread Man and were able to get a photo of it.

You want to buy the photo from me so nobody else can have it.

If I send the original digital photo to you, I can simply attach the photo to a text message and send it.

You will receive the photo.

But now, there are TWO copies of the photo. The one attached to the text message and the original file that I have stored on my computer.

What has happened is that I’ve sent you a COPY of the file of the photo, not the original file.

When it comes to sending digital photos, this may not be a big deal (unless you’re a celebrity who loves to take nude selfies and your phone gets hacked).

Imagine if Molly scanned her one-dollar bill and named the digital image, “one-dollar.jpg”.

When something is in digital form, it’s easy to copy and duplicate it…as many times as you want.

Where is the value in that?!

Molly can create an infinite number of digital copies of “one-dollar.jpg” and spend it as many times as she wants.

This issue is known as the ”double spend” problem.

If you’re trying to spend money digitally, how can you prove that the money transferred is really gone from its original place? That there was an actual change in ownership?

If Molly gives Ursula $1, how can Molly prove that she wasn’t then going to give the same $1 to somebody else?

When it comes to digital payments, the net value of all transfers needs to be equal to $0. For example, when Ursula sends $1 to Molly, Ursula should lose $1, and Molly should gain $1.

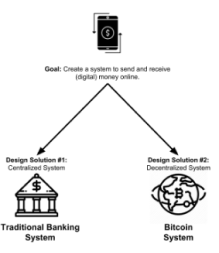

Before Bitcoin, the only way to send money electronically was through a bank or a payment company like PayPal. (And as mobile phone usage grew, fintech mobile apps like Venmo or M-Pesa.)

Basically, we had to rely on a central authority.

Here’s what happens:

If you noticed, there is no physical cash changing hands.

Instead of the physical $1 bill, Ursula and Molly rely on the bank to do a digital transaction on their behalf.

What is a ledger?

The bank keeps track of the accounts of both buyer and seller.

How does a bank keep track of its account balances?

The bank uses a ledger.

The ledger serves two functions:

In a traditional bank transaction, when Molly sends a payment to Ursula, the central authority (the bank) looks at the ledger to make sure that Molly has the funds and then decreases Molly’s bank account balance and increases Ursula’s bank account balance.

Basically, for electronic (non-physical) transfers of money, you need a recordkeeping system.

That’s what the ledger does. It keeps a record of transactions.

In this example, the ledger recorded that Molly transferred $1 (unit of currency) to Ursula. And now Molly has $0.

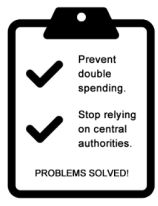

This prevents the double spending problem.

For online transactions, without these intermediaries, we could theoretically just “copy and paste” money and it’d be impossible to know which transactions were legit or fraudulent.

While relying on central authorities or intermediaries solves the “double spending” problem, this requires you to TRUST them.

For example, you must trust that your bank maintains your account balances in their ledger accurately and they don’t run off with your money or allow governments to confiscate your money.

Your transaction could also potentially be “censored” by the government, where the bank is pressured to block or reject transactions for political or other reasons.

Having to rely on and trust banks and other third parties are known as the centralization problem.

So to quickly summarise, we currently have two problems with digital money:

PROBLEM #1: Double Spending

The risk of someone being able to spend digital money twice (or more) since anything in digital format can be easily duplicated. This new amount of currency that didn’t previously exist is also known as counterfeit or fraudulent money.

PROBLEM #2: Centralization

In order to solve the “double spending” problem, you have to rely on a third party to maintain and keep track of the change in ownership of funds. But this exposes you to the risk of your digital money being stolen, confiscated, frozen, or blocked by the third party. You lose control or ownership of your money.

Satoshi Nakamoto figured out how to solve both problems!

Allowing money to move the way text messages or emails do between any two people and without any central intermediary requires a unique solution.

Satoshi’s solution created a NEW way to use money in a digital form that is counterfeit-proof and can be sent directly from one person to another (“peer-to-peer”) without having to go through a financial institution.

No more banks or other intermediaries. No more need to ask permission or get approval from them if you want to transfer money.

But how?

How the heck do you prevent double spending of digital money if you do NOT have a central authority, like a bank, maintaining a ledger and keeping track of who owns what?

Who then maintains the accuracy of the ledger?

Well, if you don’t want to rely on traditional financial institutions, you have to start from scratch and create a totally new SYSTEM.

If you want to skip the bank entirely, you need a new system for tracking value and the transferring of value from one person to the next.

Not wanting to rely on banks or governments means you can NOT be part of any existing financial system.

Why?

Because the money used in existing financial systems is based on conventional currency, also known as “fiat money” such as dollars, euros, yen, pounds, and pesos. And all of these currencies are controlled by their governments which means they are all CENTRALISED.

That’s exactly what Satoshi Nakamoto wanted to avoid. He didn’t want to rely on a central authority or administrator to manage the ledger.

This means that the system needed to be able to be operated by anyone, without the need to gain permission from some kind of gatekeeper.

The Bitcoin God wanted to use digital money that is DECENTRALISED.

This decentralisation would allow it to be a global form of money, meaning money that transcends national boundaries or governments.

It would be able to operate outside of any government regulation and central banks, which means it is not under the control of any single person or organisation.

It would be global, state-free money.

This would allow anyone to make online payments to anyone, anywhere in the world at any time.

Nobody, no company, no authority, no government could stop the transaction. (This is also known as being “censorship-resistant”.)

Satoshi Nakamoto basically wanted an online currency for the internet that would function just like physical cash (“digital cash”), that could NOT be controlled by anyone.

So what did he do?

He went to work to create a brand new system that would do just that.

This new system would be designed to manage the ownership and creation of its own unit of currency.

This new SYSTEM would allow anybody with an internet connection to send, receive, and store this “digital currency.”

This currency would exist independently from any government, central bank, or other financial institution.

This new system would be an alternative to the traditional financial system, which is built around banks.

Although many of the concepts and technologies underlying Bitcoin already existed in 2008, no one had ever put all the pieces together.

Satoshi Nakamoto took components from the previous attempts of creating decentralised digital cash and was able to combine them in a new and original way.

This new system was basically a successful Frankenstein of different technical innovations he borrowed from earlier attempts at cryptocurrencies and electronic cash in the decades before Bitcoin was launched.

Bitcoin (capital “B”) is the system that automatically manages the ownership and creation of its own digital units of currency called bitcoins (lowercase “b”).

As a Bitcoin user, you’d say that you have a certain amount of “bitcoins”, similar to how you’d say you have a certain amount of British “pounds”, Nigerian “naira”, Indian “rupees”, or U.S. “dollars”.

“BTC” has been the generally accepted currency code for bitcoin. So 1 bitcoin = 1 BTC.

One bitcoin is divisible to eight decimal places. So it’s possible to own 0.00000001 BTC.

Think of “Bitcoin” (capital “B”) as the brand name for the new system (or concept) that Satoshi Nakamoto created to move “money” around on the internet. And that “money” is denominated NOT in “dollars” or “euros” but in its own unit of account called “bitcoins”.

Why he would name the currency (lowercase “b”) as the same name as the system itself makes it obvious that he never worked in marketing. But at least now YOU know the difference!

The entire Bitcoin system is run by software that Satoshi Nakamoto created.

The Bitcoin system creates bitcoins and keeps track of the change of ownership of bitcoins.

Let’s imagine that when a $1 bill is freshly printed, the Federal Reserve, the U.S. central bank, starts tracking its change of ownership.

Whenever the $1 bill changes hands from person to person, the Federal Reserve records this on a file. The dollar bill’s entire history of ownership is constantly tracked in sequential order from its creation.

This is basically what the Bitcoin system does. But instead of creating and tracking U.S. dollars (USD), it creates and tracks bitcoins (BTC), its own unit of account.

If you send bitcoin to someone, that transaction becomes an official entry in a file that’s automatically and permanently recorded, so that bitcoin can’t be spent twice.

The file stores all past transactions permanently so that there is a complete historical trail of ownership. This is very powerful since it proves who the current owner is without needing a third party.

And there is NO central authority, like the Federal Reserve, storing and maintaining the file.

Instead, it is stored publicly by a network of computers across the world. This file is replicated and stored on thousands of independent computers and is constantly updated whenever bitcoins change owners.

Every time a transaction occurs, it is batched together with other transactions, and every couple of minutes, the ledger is updated on every computer across the network.

This means that there are thousands of identical copies of this file.

Whenever bitcoins change ownership, the transaction is recorded on EVERY one of the thousands of copies of the file around the world.

The Bitcoin system is constantly comparing all copies of the file to make sure they all have matching transactions. This ensures that all copies are kept in sync.

This “file” is Bitcoin’s ledger.

If you think about it, ANY system to keep track of digital money is just a RECORDKEEPING system.

The way banks works….keeping a central ledger…is one type of recordkeeping system.

Bitcoin is a brand new type of recordkeeping system!

Satoshi Nakamoto’s design is what allows Bitcoin to function as a recordkeeping system SEPARATE from the banks and operate totally OUTSIDE the traditional financial system.

Bitcoin does not use a central ledger. Bitcoin’s ledger is a different type of ledger known as a distributed ledger.

In the beginning, there was only Bitcoin, created by Satoshi Nakamoto.

But due to the open source nature of Bitcoin’s source code, this didn’t last.

“Source code” is the code that programmers can manipulate to change how a piece of software program or “app” works.

Open source software is software with source code that anyone can inspect, run, copy, modify, and enhance.

If you have access to a software program’s source code, you can make changes to that program such as fixing parts that don’t work correctly, improving parts to make them work better, or adding new features.

You can think of open source software like a recipe that’s available for all to see and copy.

For example, if you’ve eaten at KFC, you know how delicious their fried chicken is with Colonel Sanders’ original recipe with its 11 herbs and spices. 😋

But the recipe is secret. It’s locked in a vault (cold storage) in KFC’s headquarters. The source code (recipe) for KFC’s chicken is considered “closed source” or “proprietary”.

Since we don’t know the exact recipe, if you wanted to create the same fried chicken ourselves, you’d have to create your own recipe from scratch, probably with a lot of trial and error.

You’d end up consuming a lot of time, instead of consuming a lot of….fried chicken.

Most likely, instead of KFC, you’d end up with GFC…Gross Fried Chicken. 🤣

Now… imagine if Colonel Sanders decided to share the recipe publicly and allow anybody to use it, this would be considered “open source”.

And that’s exactly what Satoshi Nakamoto did! He deliberately shared his “recipe” (source code) with the public and published it online as open source software.

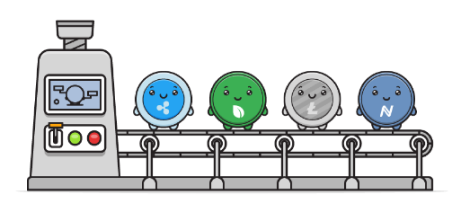

Without the need to have to reverse engineer Bitcoin’s software program and figure out how to create a cryptocurrency from scratch, other cryptocurrencies quickly emerged.

These cryptocurrencies are now referred to as “altcoins”.

What are altcoins?

What are altcoins?

“Altcoin” is a combination of two words: “alt” and “coin”. The word “alt” is short for alternative and “coin” means uh coin.

So the word, “altcoin” comes from the idea that all other cryptocurrencies are considered “alternative” coins to bitcoin (BTC), the original cryptocurrency.

Altcoins are considered to be called an alternative to Bitcoin because they are perceived to be attempts to either take the place of or improve upon Bitcoin.

A benefit of open source software like Bitcoin is that anyone in the world can take the original codebase and try to improve or extend the software’s functionality.

To give credit where credit is due, the first altcoin was Namecoin (NMC).

Namecoin’s mission was to provide a decentralised domain name service (DNS) system.

Instead of websites being limited to using domains ending with “.com” or “.net“, which were under the control of ICANN (the main governing body for domain names), it created the “.bit” domain that is independent of ICANN and could not be censored or shut down.

For example, instead of using “babypips.com” as our website URL, I could register “babypips.bit” by buying it with some NMC and use that as our URL instead.

Unfortunately, the barrier to figuring out how to actually view “.bit” websites was too high. Namecoin was really hard to use which limited its adoption. 😔

While Namecoin was the first altcoin, it definitely wouldn’t be the last.

Within a couple of years after Bitcoin’s source code was released to the public, hundreds of altcoins were born. Then thousands!

A lot of developers simply copied or slightly modified Bitcoin’s software code and then launched their own cryptocurrency. Not surprisingly, most of them weren’t able to gain any user adoption and after a couple of weeks or months, were abandoned and faded away.

Litecoin (LTC)

In 2011, Charlie Lee, a developer at Google, began experimenting with the Bitcoin source code, decided to create a “more accessible” version of Bitcoin, and named it “Litecoin“.

While Litecoin is based on Bitcoin’s source code, it has a few technical differences such as a faster transaction confirmation time (2.5 minutes vs. 10 minutes), a different hash function used for mining (Scrypt vs. SHA-256), and a larger maximum supply (84 million vs. 21 million).

Charlie Lee’s goal for Litecoin was not to replace Bitcoin but for Litecoin to be “silver to Bitcoin’s gold“.

Dogecoin (DOGE)

In 2013, Dogecoin was an altcoin that was created as a “joke” but quickly attracted and grew its own online community.

It was inspired by an internet meme known as “Doge“, a picture of a Shiba Inu dog shown in colourful text in Comic Sans font.

Due to its popularity, DOGE, Dogecoin's native currency, is considered the first “meme coin” and also the first “dog coin“.

While Litecoin was based on Bitcoin’s source code, Dogecoin was based on Litecoin’s source code.

(Are you starting to see the “benefits” of open source software? Once you’ve created something, anybody can take your work and copy it. Yay.)

Ripple (XRP)

Let’s say you’re from the U.S. and your famous significant other who is a Brazilian supermodel or footballer (your pick) wants to send you money from their bank to your bank.

There are a bunch of steps that would need to be completed, with each step usually incurring fees. And this is why international bank transfers can take days and are expensive.

Ripple wanted to change this. The founders wanted to create a platform for banks that was designed to allow international cross-border payments to be completed in seconds at a low cost.

Ripple is a company (originally founded in 2012 as Opencoin, then renamed Ripple Labs, then dropped “Labs”) that created XRP Ledger, their version of a public blockchain, which uses XRP as its native cryptocurrency.

The creators chose the ticker symbol “XRP” from the term “ripple credits” or “ripples” and the “X” prefix for non-national currencies based on the ISO 4217 standard.

Stellar (XLM)

A couple of years after Ripple was created, one of its co-founders, Jed McCaleb, created Stellar (along with Joyce Kim). While Stellar was originally based on Ripple’s codebase, it was later totally replaced.

Stellar’s goal is pretty much similar to Ripple: allow cross-border payments between any pair of currencies to be sent quickly and cheaply.

They differed in approach though as Ripple initially focused on bank-to-bank transfers, while from the start, Stellar focused on person-to-person transfers, especially from the “unbanked” (people from developing countries who lacked access to financial services).

Money transfers or remittances through the Stellar network are completed in almost real-time and at an extremely low cost.

A big difference between Stellar and Bitcoin is transaction processing speed. Stellar can process about 3,000 TPS (transactions per second) compared to 5 TPS for Bitcoin.

‘Lumens’ or XLM (originally known as “stellar”) is the native cryptocurrency of Stellar. XLM is required to pay the base fee charged by the Stellar network for any transactions.

While Stellar’s original goal was to increase financial inclusion by reaching the world’s unbanked, its priorities have shifted to helping financial firms connect through blockchain technology.

Ethereum (ETH)

One can’t talk about altcoins without mentioning (arguably) the most famous one: Ethereum.

In 2013, Ethereum was conceived to broaden the potential of blockchain technology. Prior to Ethereum, most altcoins were basically Bitcoin clones or spinoffs, designed for one very specific function…to work as an alternative “currency” outside of the traditional financial system.

Basically, the digital equivalent of cash that you can send directly from one person to another without a middleman.

For example, Bitcoin users can directly transact in BTC, Litecoin users can transact in LTC, Dogecoin users can transact in DOGE, Ripple users can transact in XRP, and Stellar users can transact in XLM. (And then exchange back to your local fiat currency if you wanted to.)

Yes, Ethereum can do the same with ether (ETH), its own native currency, but that’s not its main purpose.

What sets Ethereum apart from Bitcoin and other altcoins (back then) is that its blockchain design was more flexible and built like a software platform.

So instead of just being another “currency”, developers were able to expand the functionality of Ethereum such as having the ability to build decentralised applications (“dApps”) and even launch their own “tokens”.

Ethereum is so important that I cover it in more depth later, but for now, just know it’s an altcoin.

And one of the largest cryptocurrencies, second only to Bitcoin.

If you’ve read the previous lessons from my “Beginner’s Guide to Bitcoin Wallets“, you’ve learned what a crypto wallet is, how to set one up, and how to send and receive bitcoin.

But if you don’t have any bitcoins, how do you get some?

How do you buy bitcoin?

In order to buy bitcoin, you’ll need to open an account with a “crypto exchange”.

A crypto exchange is where buyers and sellers can trade crypto. The crypto exchange provides you with a trading platform, usually in the form of a web or mobile “app”, where you can buy and sell crypto.

Before crypto exchanges, people were only able to acquire bitcoin (and other cryptocurrencies) through mining or by negotiating individual transactions on online forums, or even face-to-face transactions in the real world.

Nowadays, most crypto beginners enter the world of crypto through an exchange. These companies make it easy for you to buy bitcoin quickly with just a couple of clicks.

There are A LOT of different exchanges operating with some more focused on beginners to the crypto markets, while others are designed for more experienced crypto traders.

Different exchanges support different cryptocurrencies so you may need to use multiple crypto exchanges depending on what you want to buy or sell.

This guide will introduce you to what crypto exchanges are and help you find one that’s right for you.

What is a crypto exchange?Crypto exchanges are websites and apps where you can exchange one cryptocurrency you own for another.

More specifically, a cryptocurrency exchange is an online trading platform where you can buy, sell and trade cryptocurrencies.

These trading platforms are defined as an “exchange” because their role is to simply MATCH buyers and sellers and are not involved in the transaction. They do charge a fee for facilitating each transaction.

Depending on the crypto exchange, you can use traditional fiat currency like U.S. dollars to buy a cryptocurrency. For example, you can buy bitcoin (BTC) with U.S. dollars (USD).

Or you can use other cryptocurrencies. For example, if you already have some bitcoins, you can buy litecoin (LTC) with your bitcoins (BTC).

In a nutshell, a crypto exchange allows you to:

What are the different types of crypto exchanges?

In general, the term “exchange” is used to describe any trading platform that allows the exchange of currencies.

But in crypto, there are actually two types of exchanges:

But which one is best for beginners? Let’s quickly do a high-level overview on both to see which option makes more sense.

A centralised crypto exchange (CEX) is typically an online business where users can create an account to buy/sell, send/receive and store native cryptocurrencies like bitcoin (BTC). This is pretty similar to forex and stock trading platforms in traditional finance (“TradFi”).

The assets on the centralised platform are under the custody of the business. Because a CEX has so much control over user funds, these businesses are usually highly regulated.

Complying with financial regulations where they operate gives them the privilege to allow users to be able to connect their bank accounts in order to fund their CEX accounts.

A decentralised crypto exchange (DEX) is where crypto traders conduct transactions directly with one another.

It is considered an alternative to traditional, centralised exchanges.

A DEX is not controlled by any one person or entity and is essentially a software program or app running on the internet.

A user would connect their self-custodial crypto wallet to a DEX to exchange or “swap” their crypto assets. Trades are executed in an automated process by the software code without the need for an intermediary.

Algorithms, coded as smart contracts, are used to determine the prices of cryptocurrencies relative to others.

Unlike CEX transactions which are handled internally, DEX transactions are settled directly on the blockchain.

Users have complete control of their crypto assets during this whole process with a DEX.

It is trustless, permissionless, and open source, all meaning that it’s open to anyone to interact with at any time.

But with no central authority and/or no government oversight of a DEX, the user can’t connect to their bank account and there is no customer service support if any issues arise.

Both CEXs and DEXs charge trading fees and the user experience is relatively simple for both platforms, although centralised exchanges are better known to have a more user-friendly experience, as well as provide customer service.

Due to the ability to deposit and withdraw fiat currency, access to customer support, and operating under regulatory oversight, I’d recommend that beginners first start with a centralised crypto exchange (CEX).

A DEX is more for advanced users and has a different set of risks. Using a DEX requires more technical skill and familiarity with decentralised finance (DeFi).

Centralised crypto exchanges (CEX) operate in different countries and support different local (fiat) currencies and different cryptocurrencies.

But they all work in similar ways. Let’s go over the steps:

To use a crypto exchange, you need to create an account. Even if you’re a wizard.

When you sign up or register for a new account, you’ll be asked to provide:

Once you’ve submitted their required information, you’ll usually be sent an email and asked to confirm your email.

Once your account is created, the next step is to “verify” your account where the main purpose is to properly verify your identity. This requires going through a “Know Your Customer” (KYC) process.

In order to buy and sell cryptocurrencies, you’ll need to verify your account and will be asked for personal information such as:

You’ll then be asked to “prove” that you are who say you are and you live where you live. This is done by asking you for:

Aside from these documents, they’ll require a selfie to make sure your current face matches the face on the ID.

Once your selfie and documents have been submitted, they will all be processed. If there are no issues, your account will be verified.

Depending on the crypto exchange, this verification process can be instant or take a few days.

Once your account is verified, you’re ready to start buying some crypto now, right? Well, not quite yet!

There’s one more step and that’s to fund your account with fiat currency.

Bank transfers, credit or debit cards, and payment apps are the more common ways to do it. Each has its pros and cons.

Let’s take a closer look at ways to “on-ramp” or convert your fiat into crypto:

Wire transfers involve filling out forms so that your bank can relay the info to a financial institution that enables the conversion of fiat to bitcoin.

Wire transfers can take a day or two (or more) depending on location. Sending moolah to a different country, for example, would take longer than if the financial institution is operating domestically.

Bank wires often incur lower fees than other options, so wiring remains popular especially if you’re an aspiring whale who is planning to buy large volumes of crypto.

Another way to send money to a financial institution is to link your bank account to it and let an Automated Clearing House (ACH) process your transfer requests.

The ACH network settles transactions in batches so transactions may take 1 to 3 business days to get approved.

Your financial institution may also limit the amount you can send or have specific cutoff times, so you’ll want to read the fine print before you choose this option.

Not willing to wait for your first bitcoin? Once you’ve made an account and have passed KYC, you can use debit or credit cards to instantly fund your account or even directly buy bitcoin and other cryptos.

The convenience is gonna cost ya though!

Debit or credit card purchases are best for low-volume transactions because fees charged by your bank, the credit card processing company, and the crypto exchange or financial institution can go somewhere from 0.75% up to 6% or even 10% of your transaction.

Ouch!

Some banks and crypto institutions also don’t allow credit card purchases. Keep close tabs on your card issuer’s restrictions as well as the crypto exchange’s minimum requirements if you’re considering debit or credit card purchases.

Once the crypto exchange has completed the transfer of the fiat deposit, your account balance will be updated and you can now buy and sell cryptocurrencies!

Some crypto exchanges will even allow you to start trading crypto “instantly”, meaning you don’t have to wait until your deposit completes.

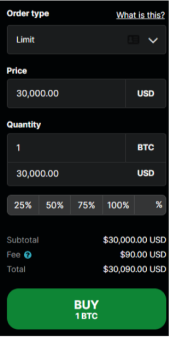

Now that your account is funded, you can use this guide to place your first order!

Similar to the forex market, crypto prices are quoted in currency pairs or “trading pairs“. And look like this:

This means that 1 unit of bitcoin (BTC) equals $1,000.

The first currency in a pair represents the base currency, while the second currency in a pair represents the quote currency.

In a Buy order: you pay the quote currency and receive the base currency.

For example, if you select “buy” BTC/USD, then you will pay in USD and receive BTC.

In a Sell order: you sell the base currency and receive quote currency.

For example, if you select “sell” BTC/USD, then you will sell BTC and receive USD.

After selecting your trading pair, in order to buy or sell, you must fill out an order form.

As long as your order has not yet been executed, you are able to cancel the order.

Any order that has been executed or canceled can be viewed under “Completed orders“.

At some point, you will want to withdraw your fiat or cryptocurrency.

If it’s fiat currency, you provide your bank account details.

If it’s a cryptocurrency, you provide your wallet address for that specific cryptocurrency.

Usually, crypto withdrawals are faster than fiat withdrawals.

In the same way, you can opt to buy bitcoin using wire transfers or ACH, these methods are also available as withdrawal options.

It’s a popular method because they incur lower fees, although the processing time can take longer.

In most cases, the withdrawal process looks like the following steps:

That’s it! Easy peasy, right?

You’ll likely need to confirm transactions via 2FA before it goes through.

The transaction could take a few hours or days to complete, depending on the crypto exchange, but you can check the pending withdrawals on your account dashboard.

After you bought some crypto, instead of selling them back for fiat, what if you want to send bitcoin (or other crypto) to an external wallet?

This is easily doable with just a few clicks and inputs!

To send bitcoin to one of your other wallets or to another user, all you need is the address or QR code of the wallet you want to send crypto to, and you’re good to go.

Just input the amount you wish to transfer and click Send. It’s as simple as sending an email!

You might also need to undergo 2FA to authorize the transaction, just to make sure that it’s really you who wishes to transfer bitcoin out of your account.

It’s the same process if you want to transfer your bitcoin to another exchange, you’ll also need the address of your wallet (for the specific cryptocurrency) on that platform.

Now that you know how to withdraw (or transfer) your crypto, it’s important that I mention one last thing…

Self-sabotage and negative thinking are common psychological obstacles that traders face, often undermining their performance and success in the market.

These mental barriers can lead to impulsive decision-making, inability to stick to a trading plan, and ultimately, loss of capital.

Let’s discuss the impact of self-sabotage and negative thinking in trading and provide practical strategies to help traders overcome these obstacles and achieve greater success.

Self-sabotage is a behavior or thought pattern that undermines or obstructs an individual’s progress, success, or well-being.

It occurs when individuals unconsciously create obstacles or engage in actions that hinder their ability to achieve their goals or maintain a positive sense of self.

It is often driven by deep-seated fears, insecurities, or beliefs about oneself, leading to self-defeating behaviors that prevent individuals from realizing their full potential.

Negative thinking refers to a pattern of thought that is characterized by focusing on the unfavorable aspects of situations, events, or oneself.

It involves a pessimistic or overly critical mindset, often leading to feelings of doubt, worry, or unhappiness.

Constant negative thinking can have detrimental effects on an individual’s mental and emotional well-being, often contributing to stress, anxiety, and depression.

Self-sabotage and negative thinking can manifest in various ways, such as:

To combat self-sabotage and negative thinking in trading, consider implementing the following strategies:

Overcoming self-sabotage and negative thinking is essential for achieving success in trading, as these mental barriers can significantly hinder performance and decision-making.

By implementing the strategies outlined in this article, traders can confront and overcome these obstacles, paving the way for personal growth and success in the market.

Remember that changing deeply ingrained thought patterns and habits takes time and persistence, so be patient with yourself and celebrate your progress as you work towards cultivating a more positive mindset.

One of the questions traders always ask me is how important trading psychology is to a newbie.

In this old man’s humble opinion, sound trading psychology is important enough that it sets consistently profitable traders apart from the rest.

A person’s ability to handle and overcome stressful situations, like experiencing a drawdown, having a losing position, and managing one’s greed, plays a central role in determining a trader’s success.

If you are not psychologically prepared to handle the stress that comes with trading, chances are that no matter how good your strategy is, you will not be able to execute it properly and will most likely see your account deep in the red.

Just take a look at the Turtle Traders’ experiment run by Richard Dennis and Bill Eckhardt.

A group of traders was taught the exact same system, with the same exact risk management guidelines and principles. Some were very successful, while others floundered.

The difference? Trading psychology.

Some of the “turtles” were unable to handle the system’s drawdowns, or closed their trades early and were unable to maximize the best trade setups.

This is very similar to handing over the keys to an F1 car to a student driver and expecting him to carve the racing track like he’s Michael Schumacher.

Even with a supercharged car, the student driver would probably lose a race to a pro driving a broken-down Honda since he likely lacks the mental fortitude to handle high speeds and sharp turns.

At the same time, we can’t overlook the importance of trading strategy.

You may be the most disciplined and emotionless trader out there, able to stick to the plan and leave emotions at the door, but you’ll probably still end up in the red if the strategy that you’re following to a T is poor and not profitable in the long run.

The key is to find the proper balance between trading psychology and strategy.

Trading psychology may not be able to turn a losing system into a profitable one, but it can equip you with the right tools to develop a profitable system.

Having the right frame of mind can provide you with valuable insights to tweak your trading approach and get better results. In effect, having the right trading psychology can lead to a better trading strategy.

Likewise, a lot can also be said about the positive effects a successful strategy can have on trading psychology. You may find that sticking to the plan and weathering drawdowns are much easier when you’re trading a tested and proven system.

To become a successful trader, you will need both the right mindset (trading psychology) and the right tools (trading strategy). Without either one, you’re bound to fail.

Analyst

The finance industry is a complex, fast-paced environment where vast quantities of data must be interpreted, processed, and converted into actionable strategies.

The role of an analyst in this context is to unravel the complexities of financial markets, decipher economic indicators, and guide trading/investing decision-making processes.

Let’s explore the intricate world of trading analysts, examining their roles, types, and how they influence the dynamics of trading.

Analysts interpret financial data, study market trends, and use economic indicators to provide investment recommendations.

Whether it’s a question of buying, holding, or selling securities, analysts offer crucial insights that guide investors’ decisions. They are, in essence, the navigators of the financial sea, helping investors traverse its often unpredictable waves.

While the overarching aim of an analyst is to guide investment decisions, there are different types of analysts, each with their unique focus and methodologies:

These analysts hone in on specific industries or sectors, studying company-specific data, industry trends, and other market factors to predict the future earnings and value of publicly traded companies. Their deep-rooted understanding of industry dynamics makes them invaluable to investors interested in specific market segments.

Often employed by investment banks, mutual funds, hedge funds, and insurance companies, financial analysts evaluate financial data, explore potential investments, and analyze economic trends. They provide a more holistic view of the market, assisting businesses and individuals in making sound investment decisions.

The world of quants is all about numbers. They employ complex mathematical and statistical models to unearth trading opportunities, value securities, manage risk, and optimize portfolios. Quants often find themselves in the employ of hedge funds and investment banks where their number-crunching capabilities are highly valued.

Specializing in risk analysis, credit analysts examine the credit data and financial statements of individuals or firms to ascertain the risk involved in lending money or extending credit. Their insights are critical in institutions like banks and credit rating agencies, where risk management is vital.

These are the pattern seekers. Technical analysts focus on interpreting historical price patterns and trends to anticipate future price movements. They make extensive use of charts, indicators, and other tools of technical analysis.

Primarily working for ratings agencies, these analysts evaluate the ability of companies or governments to pay their debts, including bonds. Their ratings can significantly impact the interest rates that companies or governments need to pay.

Analysts use various methodologies to make their assessments.

Fundamental analysis is commonly used, where a company’s financials, industry position, and market conditions are scrutinized.

Alternatively, technical analysis is applied, examining trends in a security’s price and volume.

The conclusions drawn by analysts are often simplified into ratings such as “buy,” “hold,” or “sell.”